Let’s talk about the best credit cards to use at the grocery store. Most Canadians have at least one credit card in their wallet. There are several cards in the market that provide great value at the grocery store. Having at least one of them as part of your portfolio could provide a great return on investment.

Whether you’re striving to get your finances under control, or you’re planning on taking that dream vacation, it’s important to ensure that you’re maximizing the rewards opportunities on your purchases (especially purchases of $100 or more). While receiving a low percentage of cash back, or a few extra travel rewards may not seem like it’s worth the effort, it’s important to understand that these rewards and this cashback can rack up over the year.

There are several credit cards in the market, and I’ll be the first to say that it can be daunting to know the right one for you. In the past, I’ve had a single rewards card in my wallet, and I thought this was enough. It turns out that I was getting a mere fraction of a return when comparing my rewards card to the top rewards or cash-back cards in the market.

The number of credit cards you should have in your wallet should vary depending on the individual. Someone who is a small business owner, accumulating many purchases over a year should have far more credit cards than a student.

Regardless if you have 1, 2, 5, or 10 credit cards, it’s important to have a card that offers high travel rewards, or a high cash back return at the grocery store.

The average Canadian spends $5,800 annually on groceries, so it’s important to emphasize the grocery store when focusing on your credit card portfolio.

In this post, we’ll cover the top credit cards for Canadians to use at the grocery store.

- Why You Should Use a Credit Card at the Grocery Store

- Best Overall – The American Express Cobalt Card

- Best for Cash Back – CIBC Dividend Visa Infinite

- Best No Fee Card – BMO Cashback Mastercard

- Best Visa for Collecting Aeroplan Points – TD Aeroplan Visa Infinite Privilege

- Best Card for Use at Costco: RBC WestJet World Elite Mastercard

- The Best Credit Cards to Use at the Grocery Store – FAQ’s

- Conclusion

- 4 Tips To Help You on Your Travels

Why You Should Use a Credit Card at the Grocery Store

In the fast-paced realm of modern finance, consumers are confronted with a myriad of choices when it comes to payment methods. Among these options, credit cards stand out as versatile tools that extend their benefits beyond the realms of convenience and security, especially when employed in the context of grocery shopping. As we navigate the aisles of supermarkets and make choices that impact both our well-being and financial health, the strategic use of credit cards emerges as a powerful ally in optimizing our shopping experience. In this era of evolving financial landscapes, it’s imperative to understand why using credit cards at grocery stores transcends mere transactions; it becomes a savvy consumer’s key to unlocking a plethora of advantages.

At the forefront of the rationale for favoring credit cards lies the layer of enhanced security they provide. In an age where cyber threats loom large, credit cards offer an additional layer of protection against fraudulent activities. Unlike debit cards, which are directly linked to one’s bank account, credit cards act as a buffer, shielding personal funds from potential unauthorized access. This inherent security feature affords consumers the peace of mind to shop without the constant worry of compromising their hard-earned money. Moreover, credit card companies typically employ advanced fraud detection mechanisms, swiftly identifying and resolving any suspicious activities, reinforcing the sense of financial security for users.

Beyond security, the judicious use of credit cards introduces an array of financial perks that can significantly impact one’s budget. Many credit cards offer cashback rewards, points, or airline miles for every dollar spent, effectively transforming routine grocery runs into opportunities for savings and future benefits. These reward programs, tailored to suit diverse lifestyles, allow consumers to earn back a percentage of their expenditures, presenting an attractive incentive to opt for credit over debit.

Stay up to Date on the Latest Travel Deals

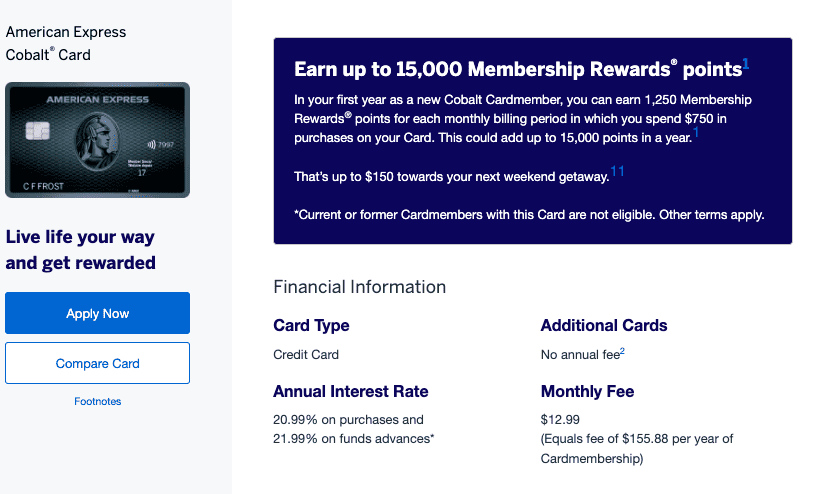

Best Overall – The American Express Cobalt Card

The American Express Cobalt Card is the premier card in the market in terms of food & beverage. Through the American Express Cobalt Card, you earn American Express Membership Rewards

American Express Membership Rewards is a loyalty program offered by American Express to its cardholders. The program allows cardholders to earn points for every dollar spent on eligible purchases with their American Express card. The points can be redeemed for a variety of rewards, including travel, merchandise, gift cards, and statement credits. Cardholders can also earn additional points through special promotions and partnerships with other merchants. The program offers flexibility in terms of how and when cardholders can redeem their points, as well as the ability to transfer points to select airline and hotel loyalty programs.

American Express Membership Rewards is a popular loyalty program among frequent travelers and those who value flexibility and choice in their rewards program, as Membership Rewards, can be transferred to several airline & hotel partners including Aeroplan, British Airways Executive Club & Marriott Bonvoy (and many more).

The cost for the card is $12.99 monthly (which comes with a $100 rebate through GreatCanadianRebates), & comes with the following benefits:

- Sign-up Bonus:

- 1,250 Membership Rewards each month you spend $500 (for the first 12 months)

- Total of 15,000 points

- 1,250 Membership Rewards each month you spend $500 (for the first 12 months)

- Earn Rate:

- 5 Membership Rewards per dollar spent on food & dining

- 3 Membership Rewards per dollar spent on streaming services

- 2 Membership Rewards per dollar spent on gas & travel

- 1 Membership Reward for everywhere else

- Insurance:

- Emergency Medical Travel Insurance – up to $5,000,000

- Lost or stolen baggage insurance – up to $1,000

- Hotel burglary – up to $500

- Car rental damage insurance

- Baggage delay insurance – up to $500

- Perks

- Occasional discounts on select products

Card Valuation

Annual Fee – $12.99 monthly fee

Sign up Bonus –30,000 Membership Rewards

Annual Spend – $500 per month for the first 12 months

First Year Value – $400

Summary

While this card doesn’t come with the best travel perks, the Cobalt is a great card to have in the wallet if you regularly shop at a grocery store that accepts American Express.

The 5 Membership Rewards per dollar spent on food & beverage is the best earning rate for any card in the market, and the relatively manageable monthly fee of $12.99 could entice Canadians to keep this card in their wallet year after year.

Best for Cash Back – CIBC Dividend Visa Infinite

For Canadians who do not frequently travel, there are still several credit cards in the market that provide ample cash-back returns at the grocery store.

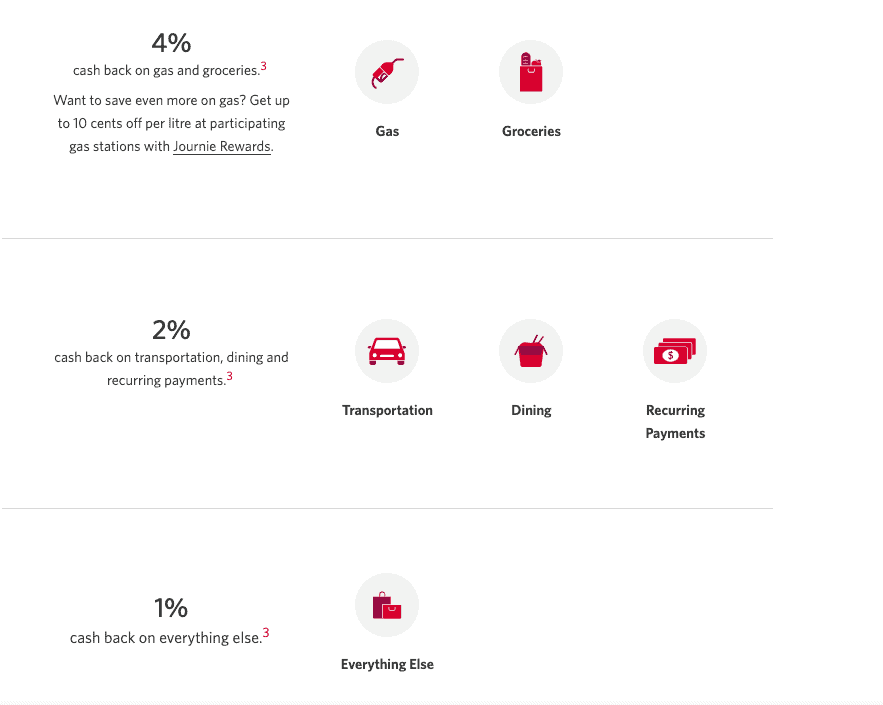

The CIBC Dividend Visa Infinite provides a 4% earn rate on gas and grocery purchases, along with strong cash back on everyday spending.

The $120 annual fee (which is rebated in the first year for new applicants) comes with the following benefits

- Earn rate:

- 4% cash back on groceries and gas

- 2% back on spending on transportation, dining & recurring expenses

- 1% on everything else

- Insurance

- Travel Medical Insurance

- Flight Delay & Baggage Insurance

- Trip Interruption Insurance

- Auto Rental Insurance

- Purchase Security & Extended Protection Insurance

- Perks

- Save up to 10 cents per liter at participating Pioneer, Fast Gas, Ultramar, and Chevron

Summary

For individuals who do not travel frequently, or don’t collect travel points, that doesn’t mean you can’t get a great return on your purchases. The CIBC Dividend Visa Infinite leads the pack in terms of cash-back opportunities at the grocery store.

Best No Fee Card – BMO Cashback Mastercard

It should be noted that several travel cards offer a first-year fee rebate. For extreme travel hackers, this could be something you should further explore, as these cards can be “churned” to receive repeat signup bonuses, and further rack up the rewards points.

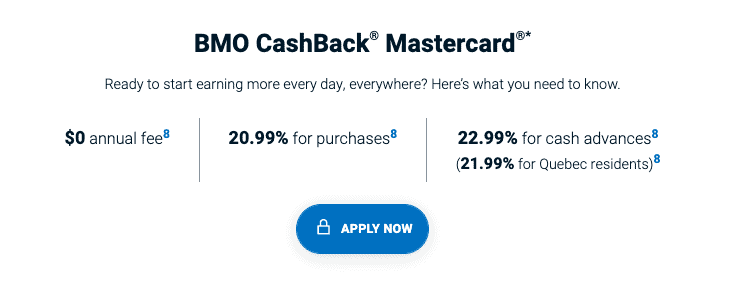

That being said, several no-fee credit cards provide you with great returns at the grocery store. The BMO CashBack Mastercard is one of the best credit cards on the market with strong cash back on groceries, along with no annual fee.

Along with no annual fee, the BMO CashBack Mastercard provides cardholders with the following benefits:

- Earn rate:

- 3% cash back on groceries, up to $500 per month

- 1% on recurring bill payments such as streaming services, subscriptions, or monthly utilities

- 0.5% everywhere else

- Welcome bonus:

- 5% cash back for the first 3 months (up to $500)

- Introductory 0.99% interest rate on balance transfers for 9 months

- Perks

- BMO Roadside Assistance

Summary

For individuals who would prefer not to carry a high number of credit cards with annual fees, the BMO CashBack Mastercard can be a great backup to the American Express Cobalt. It should be noted that the grocery store return is capped at $500 per month. If you’re part of a large family who frequently spends closer to $1,000 monthly at the grocery store, you may want to choose another card to have in your wallet.

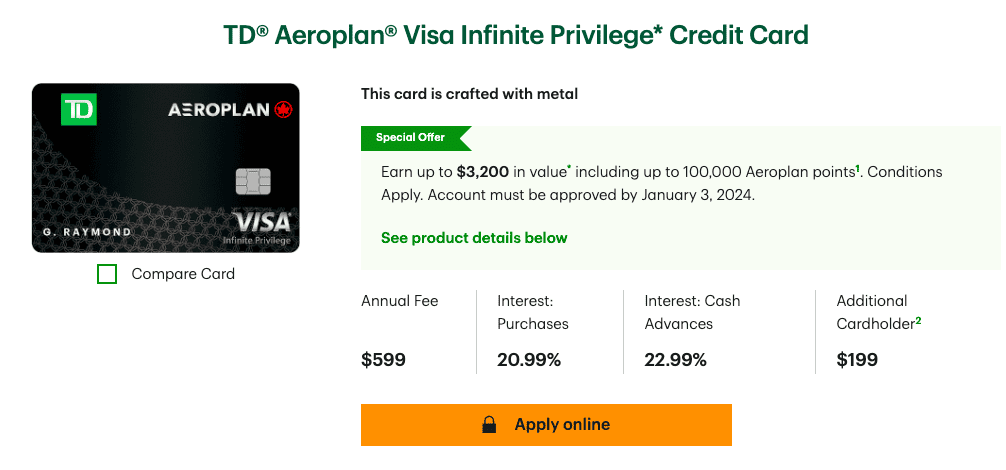

Best Visa for Collecting Aeroplan Points – TD Aeroplan Visa Infinite Privilege

For those looking to earn travel rewards for free flights, there are several credit cards in the market that allow you to achieve this, with the TD Aeroplan Visa Infinite Privilege, being the premiere Visa card in the market for Aeroplan earnings.

The TD Aeroplan Visa Infinite Privilege card is TD’s premier Aeroplan credit card

Aeroplan members can earn points by flying with Air Canada or its partner airlines, as well as through everyday activities such as shopping, dining, and staying at partner hotels. These points can then be redeemed for flights, hotel stays, car rentals, vacation packages, merchandise, and other rewards. It’s the only North American airline loyalty rewards program that offers members access to Air Canada and all Star Alliance partners. As a result, this should be your #1 focus when accumulating travel points here in Canada.

The $599 is offset by the following perks & benefits:

- Sign-up Bonus:

- 20,000 Aeroplan points at first purchase

- 50,000 Aeroplan points upon spending $7,500 in the first 6 months

- 30,000 Aeroplan points upon spending $12,000 in the first year

- Total of 100,000 Aeroplan points

- Earn Rate:

- 2 Aeroplan points per dollar spent with Air Canada

- 1.5 Aeroplan points per dollar spent on food, beverage & travel

- 1.25 Aeroplan points everywhere else

- Insurance:

- Emergency Medical Travel Insurance – up to $5,000,000

- Car Rental Insurance

- Trip Canacellation Insurance- up to $3,000

- Hotel Burglary insurance – up to $1,000

- Baggage delay insurance – up to $1,000

- Lost or stolen baggage insurance – up to $1,000

- Perks

- Priority check-in on Air Canada flights

- First bag free on Air Canada flights

- $100 Nexus credit

- Priority Airport Services at select Canadian airports

- Preferred pricing when redeeming Aeroplan points on Air Canada flights

- Earn 1,000 Status Qualifying Miles and 1 Status Qualifying Segment for every $5,000 you spend on the card

- Earn an Annual Worldwide Companion Pass after spending $25,000 on the card per year

- Lounge Access

- Maple Leaf Lounge (+1 guest)

- 6 complimentary visits to DagonPass lounges

Card Valuation

Annual Fee – $599

Sign-up Bonus – 100,000 Membership Rewards

Spend – $12,000 in the first 12 months

First Year Value – $1,900

Summary

This is the top Visa card in the market

While the $599 annual fee seems daunting initially, the 100,00 Aeroplan points will earn you potentially multiple free flights.

Canadians will have to make a personal decision as to whether or not the $599 annual fee is worth taking into the 3rd year. If you bank at TD, you can rotate through their credit card portfolios, continuously earning the signup bonus every time.

This card requires a household income of $200,000.

Best Card for Use at Costco: RBC WestJet World Elite Mastercard

Costco is a unique retailer in two ways:

- You typically buy something other than groceries during your visit to Costco

- Costco only accepts debit and Mastercard as a form of payment

If you’re comfortable holding 3+ credit cards, and you regularly shop at Costco, you should consider holding a Mastercard as part of your credit card portfolio.

The RBC WestJet World Elite Mastercard is the premier travel Mastercard in the market, which can be beneficial for use at establishments that only accept Mastercards, like Costco

WestJet Rewards is the loyalty program offered by WestJet. The program allows members to earn points on their flights, vacation packages, car rentals, and other purchases, which can then be redeemed for flights, hotel stays, car rentals, and other rewards. Overall, WestJet Rewards is designed to reward customers for their loyalty to the airline and provide them with exclusive perks and benefits.

The $119 annual fee is offset by the following benefits:

- Sign up Bonus

- 300 WSJ after your first purchase,

- 300 WSJ upon spending $5,000 in the first 3 months

- 100 WSJ as an anniversary bonus

- Earn Rate:

- 1.5% return in WestJet Dollars (with 3% return at Petro Canada gas stations)

- 2% return in WestJet Dollars when purchasing from WestJet Vacations

- Insurance

- Emergency Medical Travel Insurance – up to $5,000,000

- Car rental damage insurance

- Hotel burglary insurance – up to $2,500

- Trip interruption insurance – up to $5,000

- Perks

- A Free checked bag on WestJet flights

- Additional 20% in Petro Points on purchases made at Petro Canada

- Boingo Wi-Fi on West Jet Fligts

Card Valuation

Annual Fee – $119 annually

Sign-up Bonus – 700 West Jet Dollars

Annual Spend – $5,000 in the first 3 months

First Year Value – $660

Summary

The $600 sign-up bonus is virtually a $600 WestJet gift card, so it’s easily worth the $119 sign-up fee. The 100 WJD should entice you to keep the card into year 2.

It’s also worth noting that Petro Canada has a relationship with RBC that will allow you to save 3 cents/litre if you link your RBC debit or credit card with your Petro Points account. Needless to say, you should be taking this initial step if you own an RBC credit card.

If you currently own another RBC credit card and would like to transfer to the WestJet World Elite Mastercard, you can perform a credit card switch on the RBC banking page, or by calling their credit card hotline. Switching from one RBC credit card to another DOES NOT impact your credit score.

The Best Credit Cards to Use at the Grocery Store – FAQ’s

What if I’m concerned about paying off my credit card in time?

One of the fears about using credit cards for everyday purchases is that you don’t have insight into your purchases and that there may be a tendency to overspend. While these fears were certainly prevalent 10 years ago, modern technology can help burden this load.

- Mint.com allows you to track your spending, as you can securely link your credit card to your monthly budget.

- Every credit lender in the country will allow you to set up automatic payments with your financial institution, eliminating the fear of missing a payment.

Does using a credit card for groceries have any impact on my credit score?

Using a credit card for groceries can indeed have a positive impact on your credit score

- On-Time Payments: Making timely payments on your credit card balances, including those incurred from grocery purchases, contributes positively to your credit history. Payment history is a crucial factor in determining your credit score, and consistent on-time payments can enhance your creditworthiness.

- Credit Utilization: Credit utilization, the ratio of your credit card balances to your credit limit, is another factor influencing your credit score. If you keep your credit card balances, including grocery expenses, relatively low compared to your credit limit, it can have a positive impact on your credit score.

- Credit Mix: Having a diverse mix of credit types, including credit cards, can be beneficial for your credit score. If using a credit card for groceries is part of a well-rounded credit portfolio, it can contribute positively to this aspect of your credit profile.

There can also be some negative impacts for irresponsible spenders

- High Balances: If you consistently carry high balances on your credit card, especially in relation to your credit limit, it can negatively affect your credit score. This is known as high credit utilization and can indicate financial stress or increased risk to creditors.

- Late Payments: Missing payments or making late payments on your credit card, regardless of the type of purchase, can significantly harm your credit score. It’s crucial to pay attention to due dates and ensure prompt payment of your credit card bills.

Conclusion

Using a credit card at the grocery store transcends the realm of mere transactional convenience, offering a myriad of compelling reasons to make it the preferred payment method for savvy shoppers. The paramount importance of security cannot be overstated, as credit cards act as a formidable shield against potential cyber threats and unauthorized access, providing consumers with a robust layer of protection for their hard-earned funds. Moreover, the financial advantages woven into the fabric of credit card usage cannot be ignored.

From enticing cashback rewards to valuable points and airline miles, credit cards transform routine grocery expenses into opportunities for savings and future benefits. The intricate reward programs offered by credit card companies cater to diverse lifestyles, empowering consumers to reclaim a portion of their expenditures with every swipe.

As we navigate the dynamic landscape of personal finance, the judicious use of credit cards emerges not only as a prudent choice but as a strategic approach to elevate the grocery shopping experience. By embracing the multifaceted advantages of credit cards, consumers can navigate the checkout counter with confidence.

There are the best credit cards to use at the grocery store. In Canada, having one of the credit cards listed above in your portfolio can go a long way to maximizing the return on your monthly grocery spend. The American Express Cobalt Card provides the best overall value to Canadians, but it’s important to have another card in your wallet as well since certain retailers don’t accept AMEX as a form of payment

4 Tips To Help You on Your Travels

- These are the best credit cards to use at the grocery store in Canada. To help maximize the return on your grocery purchases, choose a credit card that emphasizes grocery store return

- If you have an American Express Cobalt Card, ensure you also have a Visa or Mastercard in your wallet in case you’re buying from a retailer which doesn’t accept Amex

- Link your credit card purchases to your monthly budgeting software to track how your spending compares to your monthly budget

- Set up automatic transfers between your credit card and your financial institution

Disclaimer: this post may contain affiliate links, meaning we get a small commission if you make a purchase through our links, at no cost to you. For more information, please visit our disclaimer page