Chequing accounts in Canada can be a great financial & travel resource if used appropriately.

As travel enthusiasts, we’re always looking to get the maximum value on our travel spend. That’s why we focus on credit card sign-up bonuses & maximizing redemptions.

Unfortunately, it can be very challenging to achieve your travel goals if your finances are all out of whack. If you have credit card debt, it can be hard to get new credit cards (and their subsequent signup bonuses). If you can’t retire, it can limit the amount of freedom you have to travel.

Simply put, a strong personal finance foundation can help you maximize the points/travel game.

The 3 pillars of building wealth are getting out of debt, spending less than you make, and saving for retirement.

When looking at saving for retirement, a Registered Retirement Savings Plan (RRSP) and a Tax-Free Savings Account (TFSA) are some of the great tools that enable you to achieve your retirement goals.

For those looking to save for a child’s education, a Registered Education Savings Plan (RESP) is another great tool that you can leverage.

However, you’re not getting paid directly into your TFSA, RRSP, or RESP. The majority of Canadians get paid directly into their everyday chequing account.

Unless you’ve been living under a rock, it’s safe to assume that you know what a chequing account is. However, based on my experience in the personal finance sector, I’ve come to the conclusion that the majority of Canadians aren’t leveraging the chequing account to its fullest potential.

High fees, stagnant savings, and inconvenient, manual processes are all some of the trends I’ve been seeing in the personal finance space when it comes to chequing accounts.

Googling “what is the best chequing account” will lead you down a personal finance rabbit hole that can be frustrating, and may result in you ditching the entire learning experience altogether. I’ve pulled a few highlights from what I consider to be great source material to help provide the benefits, and the drawbacks of the different chequing accounts in the market today.

In this post, we’ll cover 10 things you need to know about chequing accounts in Canada, that will enable you to streamline your financial objectives, hit your financial goals, and improve your travel game.

Stay up to Date on the Latest Travel Deals

Here are 10 things you need to know about Chequing accounts here in Canada

1. Understand the Function of a Chequing Account

To maximize the value of your chequing account, you need to first understand the objective of the chequing account.

Taken from Investopedia:

A chequing account is a deposit account held at a financial institution that allows withdrawals and deposits. Also called demand accounts or transactional accounts, checking accounts are very liquid and can be accessed using cheques, automated teller machines, and electronic debits, among other methods. A chequing account differs from other bank accounts in that it often allows for numerous withdrawals and unlimited deposits, whereas savings accounts sometimes limit both

So to sum it up, a chequing account is designed to have numerous withdrawals and deposits over a month.

Understanding that piece of information, let’s dive into how we can maximize your chequing account.

2. Set up Automatic Transfers

In today’s age of technology, there is very little need for you to sit around and: forget credit card payments, track your budget manually, or forget to save money for your retirement.

Your chequing account not only provides you with liquidity but also provides you with the opportunity to automatically achieve your financial wellness goals.

Credit Card Payments

I always encourage people to use credit cards if possible. There are thousands of dollars of savings/rewards available through cash back, or travel credit cards, and I think Canadians should be taking advantage of these opportunities.

One of the drawbacks I hear of using credit cards is that people will overspend, miss payments, and fall into debt. My response to this concern is that you can leverage budgeting software to track your spending (if you go over your budget, stop spending), and you can leverage technology to set up automatic transfers between your chequing account and your credit card provider. For those travelers with many credit cards on the go, these automatic transfers ensure you don’t miss a payment.

If your chequing account provider doesn’t offer this service, you may want to think about switching providers.

Budgeting

Budgeting is an important step when looking at creating personal wealth. High-end (free) budgeting platforms like mint.com can automatically sync with your chequing account, debit card, and credit card. This will allow you to track your spending on an ongoing basis

Saving for Retirement

Putting aside 15% for retirement is essential for your financial health. While some Canadians have this step taken care of by their employer through a registered pension plan, there are many of you who are saving for retirement through personal retirement vehicles (such as RRSPs or TFSAs).

You can set up automatic transfers between your RRSP/TFSA provider and your chequing account. This ensures you have checked the “save for retirement” box.

You can also set aside monthly contributions to your TFSA to help save for larger short-term purchases, or an RESP if you are building a college fund for your children.

Bottom line….a lot of this stuff can be automated

3. Don’t Let Money Sit in Your Chequing Account

There may be a few instances in your life where you need $1,000-$2,000 cash, and for whatever reason, you cannot leverage your credit card to make that purchase.

For that reason, having a few thousand dollars in your chequing account as a “24-hour emergency fund” makes sense.

Aside from that, having your money continuously built up in your chequing account makes very little sense.

Inflation is high right now, but it won’t stay like this forever. On average you can expect 6% year-over-year returns from the stock market. All this means that you are losing a great deal of money by having your money in your chequing account.

Rather than having this stagnant pool of money, you could consider:

- Paying off debt (even your mortgage)

- Building out an emergency fund with a TFSA or high-interest savings account

- Putting aside 15% for retirement into an RRSP or TFSA

- Allocating money to a Registered Education Savings Plan to help financially support your child(ren) through their higher education journey (do this if you’re regularly putting 15% away for retirement)

- Investing the money in the stock market (do this if you’re putting away 15% for retirement, individual stocks shouldn’t be your retirement plan)

- Putting the money in a TFSA to help save for short-term large purchases like a car, or rental property

- Putting money in a GIC if you are risk averse

Nowhere on this list is “have money sit and do nothing”

Your chequing account is best used as a vehicle to transfer money into funds that are going to help you achieve something impactful (like being debt-free or retiring comfortably).

4. Watch the Fees

Most chequing accounts in Canada have a monthly fee (the fees can range from $4 to $50 per month). The majority of Canadians don’t need the exorbitant price that comes with some chequing accounts in Canada. This does however depend on the individual.

To ensure you’re getting the best use of your dollars, look at the fees associated with your chequing account. Perform a quick analysis as to whether you feel you’re getting the appropriate bang for your buck.

VIP Bank Accounts & Travel Credit Cards

- If you decide that one of the “premium” bank account makes the most sense for you, make sure you’re getting the most out of the product. For example, the RBC VIP Bank Account comes with a $30 monthly fee. One of the benefits of having the account is a fee waiver on a premium credit card. This means you could own the RBC Avion Visa Infinite card at no cost. While it makes no sense to open this account JUST for the card, there’s no sense in not taking advantage of this fee waiver if you have the account.

If your bank requires you to keep more than $4,000 in the account to waive the monthly fee, consider moving banks. That money is best served earning you compounding interest in the market rather than doing nothing.

If you feel that you’re being overcharged for the services you use, call (or walk into) your bank and downgrade your premium chequing account to a basic one. OR, feel free to switch to one of the many no-fee providers that are in the market (more on those below).

I will mention that the “free” chequing accounts may make sense for some individuals, but I do encourage you to look at the fees associated with interac e-transfers, debit card transactions, and even purchasing cheques. The costs associated with these transactions may outweigh the benefits of the no-fee account.

The type of account you need is very much dependent on your usage patterns.

Review the costs, and come to your conclusion.

Overdraft Fees

Overdraft fees can be a killer, especially for those who only keep a few thousand dollars in their chequing account.

The cost of overdraft fees should factor into choosing a chequing account. If the fees are high, you may want to look elsewhere.

5. Leverage Your Bank for Travel Credit Cards

Each of the major banks in Canada offer travel credit cards. Some of these cards are in the form of an in-house travel program (CIBC Aventura for example), and some are in conjunction with a Canadian loyalty program (Like CIBC’s partnership with Aeroplan).

You should be leveraging the programs offered by your bank. There are two main benefits to doing this:

- You can “product switch” between different credit cards. When you “product switch,” you are keeping the same credit line but changing the credit card associated with it. Most of the time, this results in you receiving a portion, if not the entire sign-up bonus.

- For example, if you currently own another RBC credit card and would like to transfer to the RBC British Airways Visa Infinite card, you can perform a credit card switch on the RBC banking page, or by calling their credit card hotline.

- This allows you to keep your credit history open for a long period, ultimately increasing your credit score. If you are regularly signing up and canceling credit cards after one year, your score will go down. These long-standing lines of credit ensure your credit score remains high.

6. Ditch the Brand Loyalty

I’ve spoken with a few individuals who are under the impression that combining your chequing account with your TFSA & your mortgage will lead to savings across the board.

While in theory that makes a lot of sense, in actuality, the rebates you’ll receive are negligible.

It’s best practice to shop around for the best mortgage rates, pick a retirement vehicle that’s right for you (with a provider that’s right for you), and to pick a chequing account that makes sense for you based on the criteria above.

You will be able to leverage technology to transfer funds between your different financial institutions to ensure you never miss a payment.

For those looking to dive deeper into travel credit cards, one misconception is that you must have a bank account open with that financial institution to receive a credit card. Most banks in Canada will give you a credit card even if you don’t bank with them (although it may require an in-person visit with some institutions that are less lenient with approving applicants, TD for example).

7. Some Chequing Accounts in Canada Gather Interest

There are some chequing accounts available in the market which offer you interest on your balance.

While these interest levels are lower than what you would expect to earn in a TFSA, or through a personal investment portfolio, it still can factor into determining the right chequing account for you.

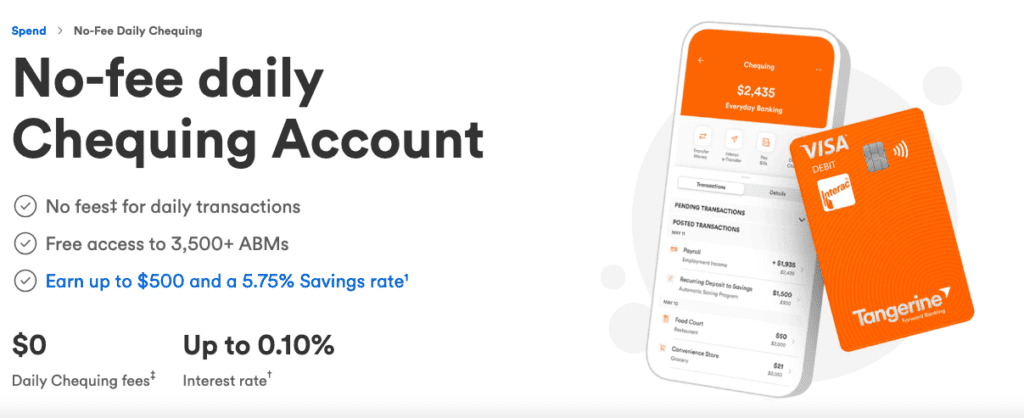

An example of this would be Tangerine’s No-Fee Daily Chequing Account

8. Chequing vs Savings Accounts

Some Canadians have questions as to whether they should keep their funds in a chequing or savings account.

As we’ve covered, the primary purpose of a chequing account is to provide you a moderate level of liquidity and to be an avenue to funnel money into accounts (TFSA, RRSP, etc) that can provide you with more long-term financial freedom.

A savings account on the other hand is meant to act as a backup to your chequing account. It’s meant to be there if you need a lump sum of cash. A savings account is not meant for daily transactions. Fees are high when using a savings account for this purpose.

In other words, a savings account is best used as an “emergency fund”

It should also be noted that several Canadians have ditched the traditional “savings” account altogether instead of TFSAs or investment accounts. The reason being is that the interest associated with traditional savings accounts is quite low compared to other investing channels.

9. Student & Senior Chequing Accounts in Canada

Virtually all banks offer student or senior rebates of 100%. If you’re a student or a senior and you’re paying for banking, call your bank and inquire as to why.

If your bank doesn’t offer free banking for seniors or students, consider moving to a bank that does.

10. Traditional vs Robo Advisors

By now, you’ve probably heard about some of the top Robo-Advisors in the market (companies like Questrade or Wealthsimple).

I’ve taken this clip directly from Investopedia to help illustrate the benefit:

In 2014, Betterment launched the world’s first robo-advisor with the aim of serving ordinary individuals who did not have enough assets to interest a skilled financial advisor, many of whom still require an account minimum of five- to six-figures and who charge 1% or more each year in assets under management (AUM). The solution was to take advantage of advances in both technology and market structure to offer low-cost and effective investing with extremely low opening balances.

On the technology side, the use of algorithmic trading, mobile apps, and digital signatures meant that the account-opening process no longer required reams of paperwork to be signed and that computers could execute trades without error and monitor portfolios continuously something that financial advisors could never be able to do for more than a handful of accounts at a time.

On the market side, low-cost exchange-traded funds (ETFs) emerged as the obvious type of securities to gain broad market exposure to various assets classes, such as stocks, bonds, real estate, commodities, and treasuries. ETFs charge very low management fees(now as low as 0.20%” when the average index mutual fund levies fees of 0.75%) and trade throughout the day like stocks, providing greater transparency and liquidity. Moreover, ETF trading has become commission-free at several brokers and clearing firms. All of this allows robo-advisors to manage client money for just 0.25% annually of AUM (on average), and users can open accounts with as little a $5.

A Robo-Advisor is Best for the Following Individuals

- Those who are technologically savvy

- Those looking to save on fees

- Entry level investors

- Those who use a traditional financial advisor or bank, but do not engage with them regularly

While robo-advisors have traditionally been associated with RRSPs & TFSAs, they are now branching into the chequing and savings space. Wealthsimple Cash is one of the new robo-advisor chequing accounts in the market

Here are a few features of this new product:

- 0.75% interest for every dollar deposited into the account

- No account fees: Wealthsimple Cash has no account minimums or, maintenance fees

- No “minimum deposit period”

- Unlimited free transfers.

- Seamlessly integrated with other Wealthsimple accounts

If you have questions about robo-advisors, or if you feel you may benefit by switching to technology-based solutions, I strongly encourage you to check out Wealthsimple.

It won’t take much research to conclude that Wealthsimple is Canada’s top robo-advisor, and it’s a product I use. Wealthsimple is different in that it’s a robo-advisor, but still provides clients with access to human advisors. It’s a best-of-both-worlds situation. Wealthsimple offers an easy-to-use platform and does not require a minimum investment to get started.

Here is a detailed review of the user experience by Canadian Youtuber Mike Griffin

Conclusion

As you may have noticed, the actual chequing account itself doesn’t have a huge impact on your financial wellness.

However, how you use your chequing account can immensely affect how quickly you build wealth. Ensuring that you can easily move money out of your chequing account to either a retirement or a high-interest savings account will help you hit your short and long-term goals.

Leveraging automatic transfers will help you keep track of your budget, and ensure you don’t miss a payment, and leveraging your current bank for their travel credit cards can go a long way to helping you see the world on points.

Chequing Accounts FAQ

Can I have multiple chequing accounts in Canada?

Yes. You can have as many as you want (although you may want to keep an eye on fees). Many families or roommates have a joint chequing account to help with bills/payments.

Many points enthusiasts have accounts at multiple banks to leverage the credit cards associated with those banks.

4 Tips to help you on your financial wellness journey

- Based on the information above, determine the chequing account that is right for you

- Link up your debit/credit card payments to your budget

- Set up automatic transfers between your credit cards and your chequing account to ensure that you don’t miss a payment

- Set up automatic transfers between your chequing account to your retirement vehicle or short-term savings account. This will help with short and long-term financial planning.

Disclaimer: this post may contain affiliate links, meaning we get a small commission if you make a purchase through our links, at no cost to you. For more information, please visit our disclaimer page