Tax-Free Savings Accounts (TFSA) can be a great savings tool for Canadians.

The 3 pillars of building wealth are getting out of debt, spending less than you make, and saving for retirement. In an earlier post, we spoke about how RRSPs can be a valuable asset when buying a home for the first time or saving for retirement.

However, RRSPs aren’t the only savings vehicle in Canada. When looking at saving for retirement, or saving for a short-term goal, a Tax-Free Savings Account (TFSA) can be a great tool in your financial wellness toolkit.

Many of us have long-term savings goals like retiring comfortably. However, short-term goals should also be built into your savings plan. These short-term goals can include a wide variety of items including:

- An engagement ring

- A second property

- A wedding

- A new car

Savings for these purchases through an RRSP won’t help financially, since the taxation when withdrawing your savings will offset any gains you made through your investments.

As a result, the government of Canada has provided Canadians with a number of great savings tools that allow you to grow your savings year over year, without having to deal with the financial burden of taxation.

For the purposes of this post, we will discuss one of Canada’s most popular savings accounts. A Tax-Free Savings Account (TFSA for short).

Googling “what is a TFSA” will lead you down a personal finance rabbit hole that can be frustrating, and may result in you ditching the entire learning experience altogether. I’ve pulled a few highlights from what I consider to be great source material to help provide the benefits and drawbacks of a TFSA.

- Here are 8 Things Canadians Need to Know About Tax Free Savings Accounts

- 1. What is a TFSA?

- 2. What are the Benefits of a TFSA

- 3. How Much Can I Contribute to a TFSA

- 4. What Type of Investments Can I Put into my TFSA

- 5. How Does a TFSA Compare to an RRSP?

- 6. How Does a TFSA Compare to a Registered Pension Plan?

- 7. How do I Open a TFSA?

- 8. What Happens if a TFSA Holder Passes Away?

- Conclusion

- FAQ’s

- 4 Tips to Help You on Your Financial Wellness Journey

Stay up to Date on the Latest Travel Deals

Here are 8 Things Canadians Need to Know About Tax Free Savings Accounts

1. What is a TFSA?

A tax-free savings account (commonly called a “TFSA”) is an assigned account by the Government of Canada for the purpose of growing your savings. It is not a specific investment like a stock or a bond.

It is designed to help individuals save money without being taxed on the growth of their investments or on withdrawals made from the account. TFSA contributions are made with after-tax income, meaning you don’t receive a tax deduction when you contribute, but the key advantage is that any investment gains or interest earned within the account are not subject to taxation.

Canadians can leverage their TFSA to help grow their savings while having that growth be tax-free. Unlike an RRSP, you are NOT subject to taxation when you withdraw funds.

With a Tax-Free Savings Account, you can withdraw your money at any time.

You can think of a TFSA like a grocery cart, and the different investment options (which we’ll get to later) as the groceries.

2. What are the Benefits of a TFSA

The #1 benefit of the TFSA is that your savings can grow in an account tax-free. Unlike an RRSP, the TFSA provides you with accessible money that you can use to fund your short-term buying goals.

Key features/benefits of a TFSA include:

- Tax-Free Growth: The income earned within a TFSA, such as interest, dividends, and capital gains, is not taxed while it remains in the account.

- Withdrawal Flexibility: You can withdraw money from a TFSA at any time, and the withdrawals are not taxed. Also, the amount you withdraw becomes contribution room that you can re-contribute in the future.

- Contribution Room: Each year, the Canadian government sets a maximum contribution limit for TFSAs. Unused contribution room accumulates and carries forward to future years.

- Wide Range of Investments: TFSAs can hold various types of investments, such as savings accounts, stocks, bonds, mutual funds, exchange-traded funds (ETFs), and more.

- No Age Limit: Unlike other retirement accounts, TFSAs do not have age restrictions. You can contribute to a TFSA throughout your lifetime.

- No Impact on Government Benefits: Income earned within a TFSA does not count toward your taxable income, which means it won’t affect your eligibility for government benefits based on income.

Having your money in a savings vehicle that will enable you to make more and pay less is infinitely greater than having your money stored away in a savings account doing nothing

There may be a few instances in your life where you need $1,000-$2,000 cash, and for whatever reason, you cannot leverage your credit card to make that purchase. For that reason, having a few thousand dollars in your chequing account as a “safety net” makes sense.

Aside from that, having your money continuously built up in your chequing account makes very little sense.

If you need to save up money for your future purchases, you should leverage the tax-sheltered savings accounts offered by the GOC.

Inflation is roughly 4%/year, and on average you can expect 6% year-over-year returns from the stock market (your TFSA). All this means that you are losing a great deal of money by having your money in your chequing account.

3. How Much Can I Contribute to a TFSA

Contribution room for your TFSA uses the following formula:

- Current Year Contribution Limit + Any Unused Contribution Room From Previous Years + Any Withdrawals Made in the Previous Year

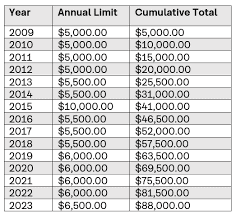

- The annual TFSA dollar limit for the years 2009 to 2012 was $5,000.

- 2013 and 2014 was $5,500.

- 2015 was $10,000.

- 2016 to 2018 was $5,500.

- 2019 to 2021 is $6,000.

- 2022 to 2023 is $6,500.

As you can see, the TFSA contribution limit for 2023 is $6,500. The lifetime limit for as of 2023 is $88,00.

The great thing is that the TFSA deposit room is cumulative, so just because you haven’t deposited money before, doesn’t mean you’re limited to 2023’s contribution limit.

For example, if you turned 18 in 2021, you have $6,000 to contribute. If you were born in 1952 and have yet to contribute, you have $75,500 of contribution room.

If you create a myCRA account, you can view your current contribution room.

Should you withdraw money from a TFSA, the amount you take out is added to how much you can contribute the following year.

Note: Growth within the plan does not count against your contribution room, losses don’t count as withdrawals.

4. What Type of Investments Can I Put into my TFSA

There are a few common investment types that Canadians can leverage within their TFSA. They include:

GICs

GICs offer a rate of return that is typically higher than a high-interest savings account, but lower than having your money invested in stocks or ETFs.

The one important factor to consider when putting money into a GIC is the need for you to access the funds. Money in a GIC is inaccessible for a predetermined amount of time (this can range from 1-36 months).

Overall – GICs are a low-risk-low-reward investment vehicle since you are guaranteed to receive your initial investment back, plus interest. The interest is typically lower than other investment options.

Bonds

You can purchase government or corporate bonds in your TFSA. Bonds are unlike GICs in that the money is accessible but similar to GICs in that the rate of return is less than stocks or ETFs.

Overall – Bonds are great for Canadians who need a low-risk savings portfolio (those closer to retirement for example). As a rule, government bonds are usually less risky than corporate bonds.

Stocks

Stocks offer a higher rate of return compared to GICs and Bonds but also come with inherent risk. Investing in stocks within your TFSA is the same as investing in stocks within a consumer platform, except your capital gains are not taxed.

Overall – Stocks are great investments for Canadians who have a higher risk tolerance, and can afford to ride out downturns in the market.

Mutual Funds

A Mutual fund chooses stocks, with the financial backing of private investors. The goal of investing in a mutual fund is to have your fund outperform the market, without having to do the legwork yourself.

Mutual funds consist of both stocks and bonds, and your financial institution should provide you with an initial questionnaire to determine your level of risk. This questionnaire should help guide which mutual funds are best for you.

Overall – Mutual Funds are great investment options for Canadians who want to passively invest (a TFSA is a great way to do just that).

Exchange Traded Fund (ETF)

ETFs trade just like a stock and consist of a basket of securities. Much like a Mutual Fund, the goal of the ETF is to outperform the market.

ETFs contain all types of investments and offer lower brokerage commissions when compared to individual stocks.

Overall – ETFs are great investment options for Canadians who want to passively invest

5. How Does a TFSA Compare to an RRSP?

Tax Free Savings Accounts (TFSA) and Registered Retirement Savings Plans (RRSP) have a number of similarities, but there are differences as well.

TFSA’s and RRSP’s both have contribution limits. Your RRSP contribution limit is tied to your annual income. The contribution limit for a TFSA however, is decided by the GOC on an annual basis.

Both the TFSA and the RRSP allow you to grow your money in the account tax-free. However, with an RRSP you will be taxed when you withdraw your funds. With a TFSA, you will NOT be taxed.

| Feature | RRSP | TFSA |

| Contribution Limit | Yes | Yes |

| Money Grows Tax Free | Yes | Yes |

| Money is Taxed at Withdrawal | Yes | No |

Taken directly from Wealthsimple:

Since both TFSAs and RRSPs are phenomenal in their respective ways, this a kind of a Batman vs. Superman question, one that begs the question why you should have an RRSP when a TFSA is similar and has no early withdrawal fees.

Here are a few of the biggest factors to consider:

- If you haven’t contributed much towards your retirement and you happen to have access to a pile of money right now through, say, a bonus, or inheritance, a TFSA might be the best option for you, since RRSPs have what’s called an annual deduction limit, meaning that you won’t be able to deduct over a certain amount in any given year. The number for 2020 is $27,230 but you can find past, current and future deduction limits on this CRA page.

- TFSA are designed to be easily accessed before retirement if the funds are needed which is good, especially for those with a more immediate goal in mind like buying a house or car. TFSAs are less good if you happen to be the type who’s never been able to resist smashing a piggy bank.

- If the funds are for your retirement, for tax reasons, TFSAs are generally considered preferable to RRSPs for those earning less than $50,000 a year.

TFSA vs Group RRSPs

Some Canadians are in a position where their employers offer a Group RRSP as a retirement vehicle.

Group RRSPs are RRSPs. where your employer is responsible for the administrative components of the plan.

Should you take advantage of your GRRSP before a TFSA?

Though GRRSPs have a few disadvantages, like limited investment options and possibly higher fees, they have one extraordinary advantage, employers will often match a portion of your GRRSP annual contribution.

If you think about the steps necessary to achieve a state of financial wellness, certain topics will come to mind like eliminating debt, reducing unnecessary expenses, and saving for retirement.

While I think those steps (and many more) should be examined on your financial wellness journey, one of the first steps that every Canadian should take is to maximize their employer’s retirement program.

Matching GRRSP plans in Canada are essentially free money for those who take advantage of the program, and taking advantage of free money should always outweigh other financial priorities other than eliminating high-interest debt.

From my experience working in the retirement planning space, GRRSPs fees are lower than what you would see from a traditional financial institution but higher than some Robo-advisors in the market. It is up to your employer to benchmark these fees against the market every few years and to do yearly investment reviews.

Maximizing your employer’s retirement offering is an easy way to make money. The program is simple to set up. Tracking your money is also easy to do. If your employer offers GRRSPs with matching, take advantage of the simplicity and ease of the program.

Given the information above, you should probably prioritize your GRRSP ahead of a TFSA, up to the point where your employer’s matching ends. At that point, you should determine if a personal RRSP or TFSA is the right retirement vehicle for you.

6. How Does a TFSA Compare to a Registered Pension Plan?

With regards to pension plans vs TFSAs, it is important to understand how much you expect to receive per year from your pension plan (there are a number of retirement calculators in the market that can help you with this).

If the projected annual retirement payout is satisfactory, you may want to look at more accessible savings accounts like a TFSA, since you can not access your pension plan until retirement. This extra liquidity may provide you with some financial flexibility.

If your projected retirement amount is less than you’re comfortable with, you’ll want to prioritize closing your retirement gap in an RRSP before putting money aside in a TFSA.

You can still receive the tax-deferred benefits through your pension contributions.

7. How do I Open a TFSA?

There are a number of establishments that offer TFSA’s including:

- Banks

- Credit Unions

- Insurance Organizations

- Online brokers (like Wealthsimple or Questtrade)

In Canada, one of the more popular trends is to open up a TFSA with a “robo-advisor”

What is a Robo-Advisor?

A robo-advisor is an automated platform or software that provides financial advice and investment management services to users. These platforms use algorithms and computer algorithms to analyze a user’s financial situation, investment goals, risk tolerance, and other relevant factors to generate personalized investment recommendations.

Robo-advisors typically operate with minimal human intervention, relying heavily on technology to manage and optimize investment portfolios. They often offer a streamlined and cost-effective alternative to traditional human financial advisors, as they can provide investment services at a lower cost due to reduced overhead and personnel expenses.

Users of robo-advisors typically start by answering a series of questions to determine their financial objectives and risk preferences. Based on this information, the robo-advisor’s algorithms create an investment portfolio tailored to the individual’s goals and risk tolerance. The portfolio might consist of a mix of stocks, bonds, exchange-traded funds (ETFs), and other assets.

Robo-advisors also often provide automated portfolio rebalancing, which involves adjusting the asset allocation over time to ensure that the portfolio stays in line with the user’s original investment strategy. Some robo-advisors also offer tax optimization strategies and automatic investment deposits to help users stay on track with their financial goals.

Robo-advisor is best for the following individuals:

- Those who are technologically savvy

- Those looking to save on investment fees

- Entry level investors

- Those who use a traditional financial advisor, but do not engage with them on a regular basis

Robo-Advisor vs Traditional Financial Advisors

| Benefits of Financial Advisors | Benefits of Robo-Advisors |

| The human element means you can call someone in case you have a question. The importance of technology is somewhat lessened. | The fees are much lower than traditional advisors, and the ease of opening a portfolio cannot be stressed enough. |

| The technology behind the algorithms eliminates the human error aspect of investing. Remember, 50% of financial advisors are below the median. Knowing that your money is being managed by a best-in-class algorithm compared to a human, instills a “set it and forget it” mentality (which is a good thing when talking about retirement planning). | The consumer-facing platforms are much easier to use compared to their traditional counterparts. |

| Most financial advisors can answer questions about topics that go beyond investment & retirement portfolios (life insurance, annuities, etc) | The consumer facing platforms are much easier to use compared to their traditional counterparts. |

Robo-Advisor Options in Canada

If you have questions about robo-advisors, or if you feel you may benefit by switching to a technology-based solution, I strongly encourage you to check out Wealthsimple.

It won’t take much research to conclude that Wealthsimple is Canada’s top robo-advisor, and it’s a product I personally use. Wealthsimple is a robo-advisor, but still provides clients with access to human advisors to answer their questions (a best-of-both-worlds situation). Wealthsimple offers an easy-to-use platform and does not require a minimum investment to get started.

Here is a detailed review of the user experience by Canadian Youtuber Brandon Beavis

Bottom line…..check out Wealthsimple

8. What Happens if a TFSA Holder Passes Away?

There are a few different factors that come into play if the TFSA holder passes away

The way the TFSA is distributed upon death will depend on either:

- The TFSA contract itself

- A will by the TFSA holder

If you are married, or in a common law relationship, you can be named as your partner’s successor, rather than a designated beneficiary. In the event of your partner’s death, you will then take over the TFSA, without taxation. This DOES not affect your personal contribution room. If you are married, or in a common-law relationship, you want to do this

for more information, please refer to this website by the CRA

Conclusion

A TFSA is a great savings option because it functions not just as a retirement vehicle, but also as an avenue to save for large purchases. These can include a car, wedding, or second property

Based on the information above, I hope you can determine where a TFSA can fit into your savings priorities.

FAQ’s

Can I use my TFSA for tax deferral?

Unlike an RRSP, a tax-free savings account cannot be leveraged for the purposes of tax deferral. The 2 main benefits of the TFSA is to:

- Have your money grow without being subject to capital gains tax

- Have your money accessible when you need it

Can I open a joint TFSA with my partner?

No, you cannot open a joint TFSA with another individual. However, if you are comfortable doing so, you can send your partner money which he or she can deposit in his/her TFSA.

This can be a beneficial practice if you’ve maxed out your contributions for the year, and your partner has not.

You can also gift money to your child, assuming he/she is over 18.

Are TFSA contribution limits cumulative?

YES, contributions are cumulative, meaning your unused contributions are rolled over to the next year.

Who Is Eligible for a TFSA?

In order to be eligible for a TFSA, you must be:

- An individual

- Have a valid Social Insurance Number

- Be a Canadian Resident

- be Over 18 years of age

Can I have Multiple TFSAs?

Yes you can, but having multiple TFSAs can be tough to track. You may accidentally over-contribute.

It is important to know the rules when transferring funds from one TFSA to another. You can perform a TFSA exchange from one to another, and not suffer any penalties. However, taking out the money from one TFSA, only to deposit it into another will count as a contribution, so you want to ensure you avoid this misstep.

4 Tips to Help You on Your Financial Wellness Journey

- Set a budget based on your monthly income, and determine what amount needs to be allocated towards your retirement (15%). Once you’ve calculated the 15%, verify your retirement income needs by using one of the many Canadian-specific retirement calculators on the internet. Double-check that your monthly allocations are sufficient to fund your desired retirement lifestyle

- Based on the information above, determine if the TFSA is the right retirement vehicle compared to an RRSP or Pension Plan

- Leverage technology to set up automatic transfers between your checking account and your retirement vehicle. This figure can be based on the numbers calculated in Tip #1

- Any leftover funds should be sent to a TFSA. These funds can be leveraged as either an emergency fund or a short-term savings vehicle

Disclaimer: this post may contain affiliate links, meaning we get a small commission if you make a purchase through our links, at no cost to you. For more information, please visit our disclaimer page