Bonds can be a great investing tool for Canadians.

Building a great investment portfolio can go a long way to helping Canadians achieve a state of financial wellness.

But for some, it’s easier said than done

Understanding the Canadian investing landscape can be challenging, and it may feel like a full-time job just to stay on top of the financial trends. Investment vehicles like stocks, bonds, ETFs, Mutual Funds, REITs, and Cryptocurrencies can sometimes overcomplicate what is a very simple process.

If you want to be a day trader, you’ll need an in-depth knowledge of these terms, but for those who are looking to build wealth and live a rich life steadily, you only need to know where the building blocks need to go, not how the building is made.

In this post, we’ll talk about one of the oldest investment options for Canadians……bonds.

Googling “What is a Bond?” will lead you down a personal finance rabbit hole that can be frustrating, and may result in you ditching the entire learning experience altogether. I’ve pulled a few highlights from what I consider to be great source material to help provide the benefits and drawbacks of bonds.

- Here are 7 Things Canadians You Need to Know About Investing in Bonds

- 1. Investing in Bonds – What is a Bond?

- 2. What are the Different Types of Bonds?

- 3. Components of a Bond

- 4. Positives of Investing in Bonds

- 5. Negatives of Buying Bonds

- 6. Investing in Bonds – Who Should Buy Bonds?

- 7. Investing in Bonds – Where Do I Buy Bonds?

- Conclusion

- Investing in Bonds – FAQ

- Personal Finance & Travel

- 4 Tips to Help You on Your Financial Wellness Journey

Terms You Need to Know

Bull Market: A bull market is the condition of a financial market in which prices are rising or are expected to rise. The term “bull market” is most often used to refer to the stock market but can be applied to anything that is traded, such as bonds, real estate, currencies and commodities (Investopedia).

Bear Market: A bear market is when a market experiences prolonged price declines. It typically describes a condition in which securities prices fall 20% or more from recent highs amid widespread pessimism and negative investor sentiment (Investopedia.com).

Fixed Income: Fixed income is a class of assets and securities that pay out a set level of cash flows to investors, typically in the form of fixed interest or dividends (Investopedia.com).

Stay up to Date on the Latest Travel Deals

Here are 7 Things Canadians You Need to Know About Investing in Bonds

1. Investing in Bonds – What is a Bond?

Let’s talk bonds. No, not the secret-agent kind, but the financial ones.

Bonds are an important part of our financial system, providing stability and security for both investors in return on their investment as well as borrowers who want to take advantage those funds at a competitive rate.

Bonds are like IOUs, but way less sketchy. When you buy a bond, you’re essentially lending money to a company or the government. In return, they promise to pay you back the original amount (the principal) at a future date, plus a little extra in interest.

Think of it as your friend borrowing 20 bucks and saying, “I’ll pay you back 25 bucks next month.” That extra 5 bucks is the interest – the incentive for you to lend your hard-earned money.

Now, the interest rate on bonds is kinda like a flirtation dance between risk and reward. Government bonds are like the dependable buddy who always pays you back but might give you less interest. Corporate bonds, on the other hand, offer more interest but come with a tad more risk – like loaning money to your entrepreneurial friend who swears they’ll make it big.

Bonds are typically less wild than stocks. They’re more of a steady-Eddie investment, providing a reliable income stream for investors. Plus, they’re great for diversifying your portfolio – spreading the risk and not putting all your financial eggs in one basket.

Oh, and the bond market is this massive playground where these bonds are bought and sold. It’s like a bustling marketplace for debts. So, when someone says, “I’m into bonds,” they’re not confessing a love for secret agents; they’re probably just financially savvy.

In a nutshell, bonds are like financial agreements where you lend money and get a little extra in return. They’re the quiet achievers of the investment world – not flashy, but dependable.

To understand the full inner workings of a bond, you will have to look for other resources (like the GOC website). BUT, you don’t need to know every detail about bonds to include them within your investment strategy.

2. What are the Different Types of Bonds?

Bonds can be issued by organizations in both the public and private sectors.

Government Bonds

If the federal government wants to issue a new project and needs the capital to pull it off, it will issue bonds to the public. Since the bond is issued by the GOC, federal bonds are one of the most reliable investments in the market (if the GOC can’t pay their bonds, we’ve all got bigger problems).

As you’ve probably guessed, the lack of risk with federal bonds is offset by a lack of growth opportunity.

Government bonds only pay out a fraction of high-paying stocks. If the stock market is yielding high results (a “bull” market), GOC bonds will perform well below the market. However, when the markets are in decline (a “bear” market), GOC bonds may outperform the market.

Government bonds can be a great compliment to stocks to ensure your whole portfolio doesn’t tank during economic pitfalls.

Investment Grade Corporate Bonds

Large corporate entities can issue bonds in lieu of stocks as a way to raise extra capital. These types of bonds are extremely secure (you must reach a certain accreditation with the Better Business Bureau to issue them), and thus have a “low-risk low reward” characteristic to them.

As is the case with government bonds, Investment Grade Corporate Bonds will perform below a bull market but may outperform a bear market.

High Yield Bonds

These bonds are released by corporations that do not meet the accreditation set by the Better Business Bureau. Unlike Investment Grade Corporate Bonds and Government bonds, these high-yield bonds have a lot more fluctuation (greater risk, potentially greater reward).

There are many financial experts who shy away from high-yield bonds. This is because you can probably get greater returns by investing in equities while taking on similar risks.

High-yield bonds are also called “junk bonds”.

Municipal Bonds

If a local government needs to raise money to support local infrastructure (maybe building a new road), they can issue bonds to the public. Municipal bonds typically yield higher earnings compared to GOC bonds.

Municipal bonds can be both investment grade (accredited), or high yield.

Gains from municipal bonds can potentially be tax-free, which can be intriguing to some investors.

Foreign Bonds

Typically foreign bonds are only purchased by investment firms or hedge funds, rather than individual investors. It may be something to shy away from as a novice investor.

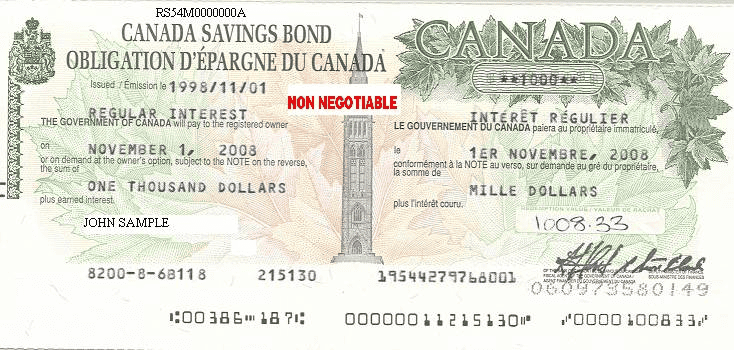

3. Components of a Bond

There are 3 main components to a bond that Canadians should be aware of:

Face Value

This is the price or cost of the bond itself. If the bond has a face value of $1,000, you are lending $1,000 to the bond issuer. This is often referred to as “the principle.”

Maturity Date

This is how long the bond is issued. Maturity dates can range from 1 year up to 30 years.

Coupon Rate

This is the amount of interest you’ll be receiving from the bond.

4. Positives of Investing in Bonds

Risk Reduction

One of the best things about buying bonds is that they are a relatively safe investment when compared to stocks, real estate & cryptocurrency. While the stock market can go up and down, bonds are relatively stable in comparison.

Diversification

We’ve all heard that a “diverse” portfolio is a good idea. Bonds can certainly help with that. Over the long haul, stocks will outperform bonds, but having bonds in your investment portfolio helps ensure that you don’t lose all your investment earnings during bear markets.

Helps the Local Economy

Buying Municipal bonds can help improve local infrastructure, and there is a certain level of satisfaction in that.

Predictability

Bonds are a very predictable stream of income. You can calculate to the dollar the amount you can expect to receive from a bond (if you purchase a $1,000 band at a 3% coupon rate, you’ll receive $30 per year from that bond). This is also called the “fixed income”

5. Negatives of Buying Bonds

Less Liquidity

Bonds require you to lock away your money for a certain period of time (depending on the bond). This can hurt your liquidity.

Less Rate of Return

The return on bonds is less than on stocks, especially in a bull market. In the long term, you will be leaving some monetary gains on the table by investing the majority of your portfolio in bonds

Issuer Default

While this is uncommon, there is still a risk of the issuer defaulting on its payments. You risk losing your investment should this happen.

Capped Upside

Due to the fixed income of a bond, your earnings are capped. A bond paying a rate of return of 3% is capped at that amount.

6. Investing in Bonds – Who Should Buy Bonds?

Whether or not bonds are a good investment depends on the individual. As a rule, there are a few commonalities among Canadians who buy bonds. Most commonly, these are risk-averse Canadians who can’t lose money.

For example:

- If you are close to retirement and can’t financially afford to lose a large chunk of your retirement savings in a stock market crash, you may want to look at a portfolio heavily invested in bonds. As a whole, people are advised to shift from stocks to bonds as they age (imagine saving up $1,000,000 for your retirement and losing half that amount at the age of 64 due to a stock market crash).

- If you are saving up for your first house via an RRSP, and your downpayment is 6-12 months away, you may want to shift your investments toward bonds. In this case, a stock market crash will severely impact the amount you will be able to contribute to the down payment.

Read >>> Your Complete Guide to RRSP’s

If your portfolio is 100% invested in stocks, you may want to leverage bonds to diversify, but once again, this depends on the individual.

7. Investing in Bonds – Where Do I Buy Bonds?

Understanding bonds can be difficult, but buying bonds is easy.

You buy bonds directly through the Government of Canada website, through your traditional financial advisor, or through any online investment platform.

If you have investments of any kind (whether online or with a financial advisor), you can buy bonds through that channel.

In Canada, one of the more popular trends is to open up an RRSP with a “robo-advisor”

What is a Robo-Advisor?

A robo-advisor is a service that uses computer algorithms to build and manage your investment portfolio. You set the parameters, such as time horizon and how much risk you’ll accept from them; then let these models do all of the hard work for you.

Robo-advisors are a great low-cost alternative to traditional investment management services.

Robo-advisors can automate investing strategies that optimize the ideal asset class weights in a portfolio for a given risk preference. Some traditional advisors are now offering robo-advisors-as-a-service as part of the portfolio construction and investment monitoring side of a more holistic financial planning practice

A Robo-Advisor is Best for the Following Individuals:

- Those who are technologically savvy

- Those looking to save on investment fees

- Entry level investors

- Those who use a traditional financial advisor, but do not engage with them on a regular basis

Robo-Advisor vs Traditional Financial Advisors

| Financial advisors tend to offer a portfolio based on face-to-face meetings rather than an online questionnaire | Benefits of Robo-Advisors |

| The human element means you can call someone in case you have a question. The importance of technology is somewhat lessened. | The fees are much lower than traditional advisors, and the ease of opening a portfolio cannot be stressed enough. |

| The technology behind the algorithms eliminates the human error aspect of investing. Remember, 50% of financial advisors are below the median. Knowing that your money is being managed by a best-in-class algorithm compared to a human, instills a “set it and forget it” mentality (which is a good thing when talking about retirement planning). | The consumer-facing platforms are much easier to use compared to their traditional counterparts. |

| Most financial advisors can answer questions about topics that go beyond investment & retirement portfolios (life insurance, annuities, etc) | The consumer facing platforms are much easier to use compared to their traditional counterparts. |

Robo-Advisor Options in Canada

If you have questions about robo-advisors, or if you feel you may benefit by switching to a technology-based solution, I strongly encourage you to check out Wealthsimple.

It won’t take much research to conclude that Wealthsimple is Canada’s top robo-advisor, and it’s a product I use. Wealthsimple is a robo-advisor, but still provides clients with access to human advisors to answer their questions (a best-of-both-worlds situation). Wealthsimple offers an easy-to-use platform and does not require a minimum investment to get started.

Here is a detailed review of the user experience by Canadian Youtuber Brandon Beavis

Bottom line…….check out Wealthsimple

Conclusion

Investing in bonds won’t lead to maximum returns, but investing isn’t about chasing maximum returns all day every day. You want to have a long-term approach, and part of that is being able to withstand the ebbs and flows in the market.

The safety net provided by bonds helps ensure you don’t feel the full wrath of a market crash.

Investing in Bonds – FAQ

Why are Bonds so Important?

At the end of the day, investing in bonds is a great way for Canadians to diversify their investment portfolio. While bonds may not get the same amount of love as stocks or cryptocurrency, they provide a certain safety net that is essential when investing.

How big this safety net needs to be depends on your risk profile. If you can financially withstand a market crash, bonds should make up only a small portion of your investments. If you need to access your investments within the next 5-10 years, you should look at transitioning a portion of your stocks to bonds.

Bonds are inversely correlated to stocks. When stocks are up, bonds are down. When stocks are down, bonds are up. Bonds help ensure that there is never a period where ALL of your investments are losing money.

What Percent of My Investment Portfolio Should be Bonds?

This is why I love Robo-Advisors like Wealthsimple. They will automate your investments based on your risk profile. If you have a lower risk tolerance, they will skew your investments more towards bonds.

It’s an extremely easy way to ensure your investment strategy is appropriate, while also saving on fees. Robo-Advisors can also adjust the percentage of your portfolio invested in bonds over time.

If you’d prefer more of an active approach to investing, a general rule of thumb is that no less than 20% of your investment profile is in bonds/fixed-income. As you progress closer to retirement, this number should increase.

What’s the Deal With Bond Ratings?

Agencies like Moody’s or S&P assign ratings to bonds indicating their creditworthiness. AAA is top-notch, while lower ratings suggest higher risk.

Are There Tax Implications With Bonds?

Yes, the interest income from bonds is generally taxable, but government bonds may have tax advantages.

Personal Finance & Travel

Having a good personal finance setup can positively impact someone’s ability to travel. Here are a few ways in which personal finance can play a crucial role in enabling travel:

- Savings and Budgeting: A well-managed budget allows individuals to allocate funds for various expenses, including travel. By saving consistently and setting aside money specifically for trips, people can afford to travel without compromising their financial stability.

- Emergency Fund: Having an emergency fund provides a financial safety net. In case of unexpected expenses or emergencies while traveling, individuals with a well-established emergency fund are better equipped to handle such situations without derailing their overall financial plan.

- Credit Score and Cards: A good credit score opens up opportunities for obtaining travel-friendly credit cards. These cards often come with benefits such as travel rewards, cash back, or airline miles, which can significantly reduce travel costs when used wisely.

- Debt Management: Minimizing and managing debt is crucial. High-interest debt can be a significant financial burden. By prioritizing debt repayment and maintaining a healthy credit profile, individuals can avoid unnecessary financial stress and potentially qualify for better loan terms if needed for travel-related expenses.

- Investments: Investing wisely can contribute to building wealth over time. Returns from investments can be used to fund travel or supplement one’s income, providing more financial flexibility for leisure activities.

- Income Streams: Diversifying income streams or pursuing additional sources of income can boost overall financial stability. This additional income can be earmarked for travel, allowing individuals to explore new destinations without compromising their primary financial goals.

- Cost-Effective Travel Planning: A good personal finance setup encourages smart travel planning. This includes researching and taking advantage of discounts, using travel rewards, and making cost-effective choices in accommodation, transportation, and activities.

In summary, a solid personal finance foundation, including savings, budgeting, emergency preparedness, and smart financial habits, can positively influence an individual’s ability to travel by providing the necessary resources and financial security.

4 Tips to Help You on Your Financial Wellness Journey

- Determine the investment vehicle that’s right for you (TFSA, RRSP, RESP).

- Use the tax-advantaged accounts offered by the Canadian government to help reduce your taxation.

- Conclude whether or not you should be investing in a traditional or a robo-advisor.

- Ensure that bonds are a part of your investment portfolio (the amount should vary based on your risk tolerance). Investing in bonds reduces the overall risk of your portfolio.

Canadian Investment Series

Read >>> Investing in ETFs

Read >>> Investing in Stocks

Disclaimer: this post may contain affiliate links, meaning we get a small commission if you make a purchase through our links, at no cost to you. For more information, please visit our disclaimer page